Tired of complicated finance apps you stop using after a week? Here's what makes a personal finance management app actually work and why most people quit before seeing results.

Managing money shouldn't feel like a part-time job. But most personal finance apps make it exactly that. Complicated dashboards, endless manual entry, features you never use.

You download the app, set it up, use it for a week, and never open it again. Tracking your finances should take seconds, not hours.In this blog we'll show you what makes a personal finance management app actually work and why simplicity beats complexity every single time.

Why you'll Quit Personal Finance Apps in Two Weeks

Here's something nobody talks about. The personal finance app industry has a massive dropout problem. People download these apps with good intentions. They set up their accounts, link their banks, create budgets, customize categories. And then life happens.

The app sends a notification. You ignore it. A few transactions pile up that need manual categorizing. You skip a day. Then two. By week three the app is just sitting on your phone collecting dust.

The problem isn't motivation. It's friction. Every second of manual effort is a reason to quit. And most personal finance management apps are loaded with friction. They ask you to type amounts, pick categories from dropdown menus with 47 options, manually tag transactions, and reconcile accounts. That's not managing your finances. That's doing data entry for free.

3 Things Your Personal Finance App Must Do

If you strip away all the fancy features that look good in screenshots but nobody uses, a good personal finance app only needs to do three things well.

Show you where your money goes. Not in a pie chart you'll glance at once. In clear, simple categories that make sense. Food. Transport. Bills. Shopping. You should be able to open the app and know within 5 seconds what's eating your budget.

Make tracking automatic. The moment you have to type something manually, the clock starts ticking on when you'll quit. The best app is one that does the work for you. You give it the data (a receipt, a bank statement) and it handles the rest.

Keep it simple enough to use daily. If an app takes more than 10 seconds to log an expense, it's too slow. People track expenses at the checkout counter, in the car, between meetings. The app needs to match that speed.

Everything else, investment tracking, bill reminders, subscription management, those are nice to have. But if the basics don't work fast, none of the extras matter.

Reason why you Don't Know Where Your Money Goes

Most people think they have a spending problem. They usually don't. They have a visibility problem.

You buy coffee every morning. That's about $4 to $5. Doesn't feel like much. But that's $120 to $150 a month. Add in the random snacks, the Uber rides you could've skipped, the subscriptions you forgot about. Suddenly $500 to $700 has disappeared and you genuinely can't explain where it went.

This happens because small daily purchases are invisible unless you track them the moment they happen. Checking your bank balance at the end of the month tells you the total damage but not the cause. It's like weighing yourself without knowing what you ate. The number means nothing without the breakdown.

A personal finance management app that categorizes every expense automatically fixes this. You stop guessing and start seeing patterns. And once you see that you're spending 35% of your income on food, your brain starts making different decisions on its own. You don't even have to force it.

Will Tracking Expenses Actually Change my habits?

Most people notice a shift in their spending habits within the first month. Not because the app told them to spend less. But because seeing your money broken down by category changes how you think about purchases.

A survey of expense tracking app users found that people who tracked daily expenses for 30 days reduced their unnecessary spending by 15 to 20% on average. Not by following a strict budget. Just by being aware.

The trick is surviving those 30 days without quitting. Which brings us back to the same point: the app has to be easy enough that you actually use it every day.

Simple VS Useless? Difference in Finance Apps

There's a difference. A simple app removes unnecessary steps but still gives you useful data. A basic app just doesn't do enough.

Here's where that line sits:

Useless: You type your expenses manually into a list. No categories, no reports, no insights. Just a glorified notepad.

Too complicated: You spend 20 minutes setting up budget categories, linking three bank accounts, customizing notification preferences, and watching tutorial videos before you can log your first expense.

Simple and useful: You scan a receipt or upload a bank statement. The app reads the data, categorizes it, and shows you a clear picture of your spending. No setup. No learning curve. Open it, use it, done.

That middle ground is where a personal finance management app actually works long term.

Can I Catch Up on Old Expenses?

This is a question that stops a lot of people from starting. They think "I've already missed months of expenses, what's the point of starting now?"

The answer: you don't have to start from zero. If you have bank statements (and everyone does), you can upload them and have every past transaction categorized automatically. That gives you months of spending data without scanning a single receipt.

Going forward, you just scan receipts as you get them. The combination of past bank statement data and daily receipt scanning gives you a complete picture of your finances.

What About Couples and Families?

Money is the number one thing couples argue about. And it's usually not about how much they earn. It's about not knowing where it all goes.

When both people in a relationship track their expenses, the arguments get replaced by conversations. You're not blaming each other for overspending when you can both see the exact breakdown. "We spent $800 on eating out this month" is a fact, not an accusation. And facts are easier to work with than feelings.

A good personal finance management app should make it easy for both people to scan receipts into the same account. That way your monthly spending picture is complete, not just one person's version of it.

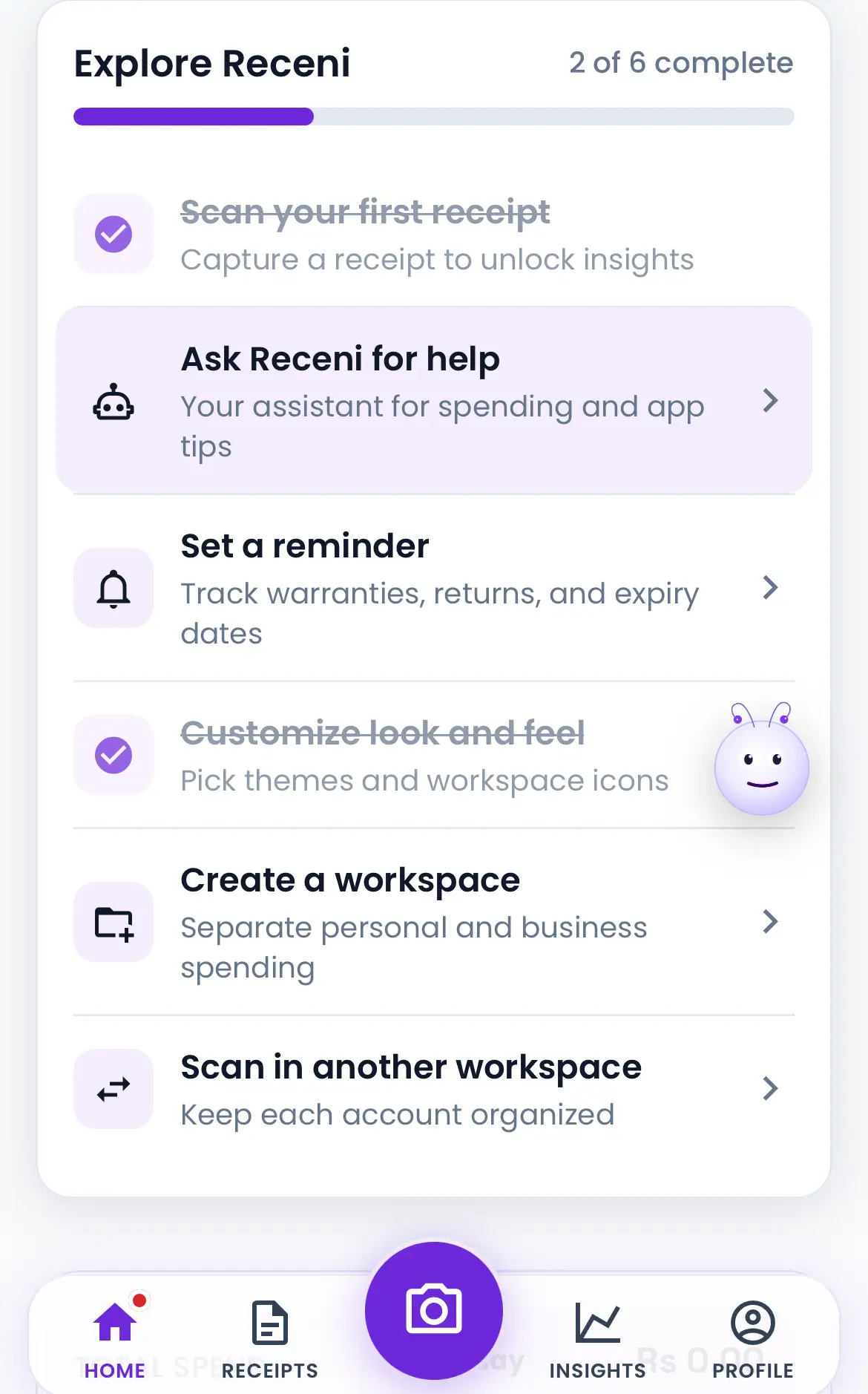

How Receni Makes All of This Simple

We built Receni after watching people (including ourselves) fail at expense tracking over and over. The problem was always the same. Too much manual work.

So we stripped everything down to the simplest possible version of expense tracking that still gives you real value.

Scan any receipt in 3 seconds. Point your phone camera at a receipt. Receni's AI reads the amount, tax, category, vendor, and date. All extracted instantly. No typing.

Scan up to 4 receipts at once. Got a pile of receipts? Lay them out, take one photo. Receni detects each receipt separately and extracts data from all four individually.

Upload bank statements. Don't have receipts for past months? Upload your bank statement and Receni converts every transaction into a categorized receipt automatically. Months of untracked expenses organized in seconds.

Auto-categorization. Every receipt gets categorized automatically. Food, transport, bills, shopping. You can see exactly where your money goes without setting up anything.

Budget limits. Set monthly spending limits by category. Receni shows you how close you are so there are no surprises at the end of the month.

Free to use. Receni is free on App Store and Google Play. No trial period, no credit card required.

The Only Thing That Matters

Every personal finance management app promises to help you manage your money. But the only app that actually helps is the one you're still using after 30 days. And the only way you'll use it for 30 days is if it takes almost zero effort.

That's what we optimized for at Receni. Not more features. Less friction.